+(1).png)

Fortuna Silver (FSM/FVI.TSX) has finally commissioned its much awaited Seguela Project, a move that has given it a fifth operating asset, and its largest and lowest-cost asset in its portfolio. This is because Seguela is expected to produce ~135,000 ounces per year for its first six years at all-in sustaining costs below $950/oz when account for inflationary pressures. And while the reserve base at Seguela might seem small at just ~1.1 million ounces, drill success at the Sunbird deposit will lift overall reserves, with an updated resource/reserve and life-of-mine plan [LOMP] expected by year-end. In this update, we'll dig into recent exploration at the mine and whether the stock is offering enough margin of safety after its ~65% correction over the past 2.5 years.

(Source: Company Website)

All figures are in United States Dollars unless otherwise noted.

Seguela 2021 TR & Upcoming LOM Extension

Fortuna's new Seguela Mine envisioned operating a high-grade open-pit over a 9-year mine life, with a throughput of ~1.3 to ~1.6 million tonnes per annum, producing ~120,000 ounces of gold over a 9-year mine life. This was based on a reserve base of ~1.09 million ounces of gold at 2.8 grams per tonne of gold, but this reserve base including just five deposits: Ancien, Agouti, Boulder, Koula and Antenna. However, since then, the company has added a sixth deposit in Sunbird, a discovery that was made in 2021 that blossomed to a 350,000 ounce inferred resource in Q1 2022 before a doubling of its resource to 758,000 ounces in Q4 2022 with ~279,000 ounces moved into the indicated category.

Since then, Fortuna has continued to enjoy drilling success, with infill holes continuing to deliver solid intercepts including the following:

- 18.9 meters at 12.7 grams per tonne of gold

- 8.4 meters at 16.2 grams per tonne of gold

- 13.3 meters at 4.7 grams per tonne of gold

- 5.6 meters at 10.7 grams per tonne of gold

A look at the deposit after recent drilling suggests that Sunbird has room to potentially extend the pit slightly to the north with moderate grades near Section 893,600, and there also appears to be an opportunity to deepen the pit or look at underground mining, with some high-grade mineralization poking out of the bottom of the resource bottom. This is also an opportunity at Ancien, where high grade mineralization has also intersected at depth. However, there appears to be some moderation in grade vs. previous expectations in the ~893,400 section, with the previous drill plan showing higher grades in this area than we're seeing presently. This is not a big deal, and Sunbird still looks like it should be a 750,000+ ounce resource at 3.0+ grams per tonne of gold, translating to a ~525,000 ounce reserve, assuming a 70% conversion rate on all ounces (M&I and inferred).

Assuming this is the case and accounting for half a year of mining depletion, Seguela's reserve base should grow to ~1.6 million ounces, translating to over 3 years of additional mine life assuming no increase in throughput to take advantage of this reserve growth. This is a very positive development as it will not only boost project NPV, but the high-grade Sunbird material might displace lower grade ore at Boulder and potentially top up feed grades in the back half of the mine life, allowing for higher feed grades in Year 7 through 9 vs. the ~1.93 gram per tonne average expected in the 2021 TR. Overall, I see this as having a positive impact on NPV at Seguela, though I have already accounted for most of this upside as I was originally expecting at least 600,000 additional reserves ounces from Koula, Ancien and Seguela by 2025, with the potential to pull some of these ounces forward in the mine life.

As for the bigger picture, the growth in reserves at Seguela is certainly positive, but the issue is that Yaramoko is sitting with barely a 3-year mine life and Burkina Faso is not getting any more attractive as a jurisdiction. Meanwhile, Lindero may have a longer mine life, but the best years of this mine are in the rear-view mirror and inflationary pressures are not helping this high-volume and low-grade operation that's quite sensitive to energy prices. Finally, I'm struggling to remain optimistic about San Jose, an asset that has seen limited reserve replacement and could see even higher cut-off grades (creating an increased hurdle to adding new ounces) from the rising Mexican Peso, pressure on higher profit-sharing at Mexican mines, and continued consumables inflation, which could ultimately lead to higher cut-off grades in the 2023/2024 reserve update.

(Source: Company Filings, Author's Chart)

(Source: Company Filings, Author's Chart)

So, while it's nice to see one asset growing reserves, the trend is likely to be continued reserve declines across the portfolio on a consolidated basis, which ultimately means lower production as Yaramoko and San Jose will likely be winding down by H2 2026 or earlier (more than offsetting the production growth from Seguela).

Recent Drill Results

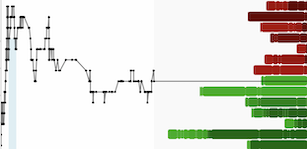

While the upside to the Seguela LOMP is positive with the company likely to report closer to a 14-year mine life (albeit at higher costs than the ~$830/oz estimates initially to account for inflationary pressures), the other excitement was around new targets, which we learned about in December 2022. Two of these targets that have received follow-up drilling are Badior and Barana, which lie north of the plant and a similar to Ancien (~8 kilometers away). And while the initial results were very encouraging (as was the recent highlight intercept of 1.8 meters at 90.9 grams per tonne of gold from Barana), the average hole hasn't met my expectations, with relatively minor widths, moderate grades and less impressive continuity. This point is highlighted in the below charts, which show all intercepts released at Barana and Badior at or above 1.0 meter in true width.

(Source: Company Filings, Author's Chart)

Beginning with Badior, Fortuna released over 20 intercepts to date, with ~70% having no significant intercepts, equating to economic mineralization. This is a relatively low hit rate and has underperformed my expectations. It's possible that the company simply hasn't got a good handle on the mineralization yet, but the lower hit rate is a little disappointing even if there have been a few decent intercepts released from this prospect. As for Barana, we've seen 30 intercepts released, and while the hit rate was better at ~60%, there were still 12 intercepts labeled as having no economic mineralization. Meanwhile, if we cut out the best intercept (1.8 meters at 90.9 grams per tonne of gold or 80 when top-cut), the remaining intercepts averaged 4.6 meters at 2.0 grams per tonne of gold, which is nothing like what we see from Sunbird which is regular 10+ meter intercepts at 3.5+ grams per tonne of gold.

(Source: Company Website)

Given that these were potential bonus ounces for Seguela at these two prospects, I don't see this as a negative to the investment thesis, but I haven't been all that impressed with these two prospects, with the second batch of results being weaker than the first, especially if we count the high-grade intercept as an outlier (which it clearly is based on the chart). Obviously, I could be wrong here and the low future cut-off grade for reserves (0.65 - 0.70 grams per tonne of gold after accounting for inflationary pressures at regional targets) suggests that there's a low hurdle to adding new ounces. However, regarding these prospects, I'm less excited than I was previously, so investors may have to hope for more consistent results out of Gabbro North and Kestrel for adding a potential seventh deposit to the mine plan.

So, how does Fortuna's valuation look?

Valuation

Based on ~310 million fully diluted shares and a share price of US$3.05, Fortuna trades at a market cap of ~$946 million and an enterprise value of ~$1.14 billion. This is a much more reasonable valuation than over a year ago when I warned against paying up for the stock at US$4.30. And for a company with a diversified portfolio of five mines in multiple jurisdictions, this might seem like a steal. However, as I've detailed in past updates, West African gold producers trade at massive discounts to their peer group, and Fortuna has arguably morphed into a West African producer, with over 60% of NAV and gold-equivalent production tied to Africa.

Using what I believe to be more conservative multiples of 5.0x forward cash flow and 0.90x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see a fair value for Fortuna of US$4.30. This points to a 40% upside from current levels, but I am looking for a minimum 40% discount to fair value to justify owning small-cap producers based primarily in Tier-2/Tier-ranked jurisdictions (Mexico, West Africa, Argentina, Peru). After applying the minimum discount, the ideal buy zone for the stock comes in at US$2.60 or lower, suggesting that FSM has still not yet moved into a buyable position. Obviously, I could be wrong and the stock could head higher without entering this buy zone. However, I've never found any value in investing in depleting businesses in riskier jurisdictions unless a material margin of safety was present, and with more diversified producers that are returning value to shareholders also trading at attractive multiples like B2Gold (BTG/BTO.TSX) but with Tier-1 exposure, I see several more attractive bets elsewhere currently.

Some investors may disagree with this view, pointing out that Fortuna is steeply undervalued relative to peers on a P/CF and EV/EBITDA basis according to its most recent presentation. However, these charts can deceive if one doesn't read the fine print. And while the company does trade at a discount to its peer group, I would argue that it has conveniently chosen its peer group to include some of the lowest-cost producers sector-wide like Lundin Gold (LUGDF), Alamos Gold (AGI), and Dundee PM (DPMLF), several Tier-1 jurisdiction producers, larger producers like SSR Mining (SSRM), and silver producers. And with only one West African producer in the peer group and Fortuna hardly being a silver producer with the bulk of its revenue from gold (and less so than most of its silver producer peers), it's no surprise that it trades at this "discount".

However, if we stack the company up against a more relevant comparison, Perseus (PMNXF/PRU.TSX), the stock is actually more expensive than Perseus (~4.0x EV/CF vs. ~3.0x EV/CF despite Perseus having a better balance sheet and much lower operating costs (sub $1,075/oz AISC).

Disclosure: I am long BTO.TSX/BTG

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.