Link to Original Article: https://www.smallcapinvestor.ca/post/we-cannot-electrify-the-world-without-uranium-copper

URANIUM

We are only two weeks into the new year and uranium continues to shine brighter than every other sector. Despite uranium prices increasing by over +85% last year, the trend does not look to be slowing down any time soon, with prices pushing up over $100/lb to start the new year off. This is the highest that uranium has traded since 2007.

Increasing Demand

The global decarbonization drive and the ructions in energy markets in the wake of Russia’s invasion of Ukraine have helped spark a renaissance in the nuclear industry, with governments increasingly willing to sign off on new projects despite cost over-runs and delays that continue to plague the sector. The World Nuclear Association has updated their data on 61 new reactors currently under construction worldwide which will add 68 Gigawatts of new electricity generation and about 34M lbs/yr more uranium fuel demand, with 24 coming online in 2024/2025.

The Supply Gap

Given how much the uranium price has increased, it would be natural to assume that the largest uranium producers would start increasing production; however, this is not the case. On January 12th, the world’s largest Uranium miner, Kazatomprom, warned that it may miss production targets for the next two years due to the challenges related to the availability of sulphuric acid, a critical operating material, as well as delays in completing construction works at the newly developed deposits. In 2022, Kazatomprom accounted for 23% of the world’s uranium supply.

Forecasts project a persistent supply-demand imbalance for uranium, with an anticipated cumulative gap of approximately 680,000 metric tons by 2040. Meanwhile, the existing supply gap is expected to intensify, signifying a prolonged shortage in the market.

BofA's metals and mining team said tightness in uranium markets could extend well into 2025, indicating that prices could run higher through this year. The team of analysts has increased their uranium spot price targets to $105 per pound in 2024 and $115 in 2025.

They outlined three near-term catalysts that could propel prices higher:

- Higher electricity prices make higher uranium prices more absorbable

- Investment fund volumes continue to increase

- Inventories are lower than previously thought while production slippages also remain a risk

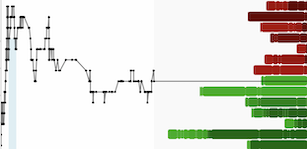

While uranium equities were lagging behind spot prices for the first week of the year, they have started to play catch up in a big way.

Below is a short list of uranium equities and their performance so far in 2024:

COPPER

The thesis for rising copper prices is pretty simple.

The essential role of copper in the construction of electric vehicles, power grids, and wind turbines is a key factor set to propel a price increase, with forecasts pointing towards a potential rise to $15,000 per tonne in 2025. The escalating demand for copper, notably from nations like Chile and Peru, underscores the imperative for augmented mining investments. This heightened investment is crucial to address the burgeoning global requirements arising from the transition to renewable energy. In addition, hinderances to supply from several huge copper mines across the globe such as Cobre Panama, has caused a downward revision in copper supply.

Copper Market Dynamics: From Surplus to Soaring Prices in 2024 Amidst Green Transition Acceleration

In Autumn 2023, the International Copper Study Group (ICSG) initially forecasted a significant surplus in the copper market for 2024 due to increased global production. However, updated predictions at the year's end indicated a potential surge in copper prices for 2024, driven by global deficits resulting from ambitious climate pledges. The ICSG estimated a surplus of 467,000 metric tonnes, but emphasized the evolving supply-demand dynamics amid the accelerating global green transition.

The October update highlighted weak Western demand and robust Chinese copper output, with non-China usage expected to decline by one percent. Chinese demand, driven by power and electric vehicle sectors, was projected to grow by 4.3 percent in 2023. The ICSG anticipated improved manufacturing activity, ongoing energy transition, and new capacities to support higher global refined copper usage in 2024.

By the end of 2023, a report from BMI Fitch Solutions suggested a dramatic rise in copper prices over the next two years due to supply disruptions and increased demand, expecting a more than 75 percent increase. The prediction considered mining disruptions, higher demand from global green initiatives, and a potential decline in the U.S. dollar value.

Industry Experts Weigh In

I spent my weekend listening to a few different podcasts from commodities experts and natural resource industry veterans. One of them was the Smarter Markets Podcast from Abaxx Technologies which featured special guest Jeff Currie, former Global Head of Commodities Research at Goldman Sachs.

“You cannot electrify the world without copper and we simply don’t have enough of it,” he said. In particular, he notes the enormous amount of earth that needs to be moved in order to extract a relatively small amount of metals and that in today's copper mines, 0.3% is a very common grade for ore deposits.

Listen here:

https://x.com/num8ersguy/status/1746255137189089325?s=20

I also listened to a great podcast from Wealthion which featured the legendary Pierre Lassonde as a special guest. Pierre also sees copper rising another 10-20% this year as we move to decarbonize and electrify the planet.

https://x.com/num8ersguy/status/1746658383057576106?s=20

Presently, about 80% of the global energy powering our systems comes from carbon-based sources such as petroleum, oil, and coal, with the remaining 20% sourced from alternative means. To achieve the ambitious goal of decarbonizing our world, a significant shift is necessary—reversing those percentages to ensure that 80% of our energy derives from non-carbon sources. Realizing this transition requires the expansion of electricity distribution systems, predominantly reliant on copper.

Copper is the linchpin in various aspects of our infrastructure, from buildings and air conditioning to elevators and transportation. To meet the escalating demand for copper in the next two decades, we must double our current copper production. While there are notable mining projects set to contribute to production in the next 1-2 years, a looming deficit in copper supply awaits beyond that period.

The Bottom Line

The outlook for both uranium and copper presents a compelling narrative for the global energy landscape. Uranium's remarkable surge, driven by increased demand for nuclear energy amid global decarbonization efforts, positions it as a standout performer. Forecasts indicating a persistent supply-demand imbalance and potential price hikes, coupled with near-term catalysts outlined by BofA's metals and mining team, suggest a bullish trajectory for uranium prices well into 2025.

On the other hand, the copper market dynamics highlight the indispensable role of copper in the transition to renewable energy. Despite initial projections of a surplus, the evolving landscape, marked by increasing Chinese demand, supply disruptions, and a global green transition, points towards soaring copper prices in 2024. Industry experts, including Jeff Currie and Pierre Lassonde, emphasize the criticality of copper in electrifying the world, underlining the necessity for substantial mining investments to meet the escalating demand.

As we navigate the transition towards decarbonization and electrification, both uranium and copper emerge as pivotal elements in shaping the future of our energy infrastructure. The challenges in meeting the growing demand for these essential metals underscore the urgency for strategic investments, technological advancements, and international cooperation to ensure a sustainable and resilient energy future.

Disclosure

The author did not receive any compensation for publishing this article. While the author has made reasonable efforts to ensure the accuracy and reliability of the content, readers should conduct their own research and analysis and seek independent financial advice before making any investment decisions.